When it comes to planning for retirement, one of the most important decisions you'll make is how to save for your future. Investing in an Individual Retirement Account (IRA) can offer significant tax benefits, but choosing between a Roth IRA and a Traditional IRA can be confusing. Both types of IRAs have unique advantages and disadvantages, which can impact your long-term financial strategy. In this article, we'll delve into the key differences, helping you to make an informed decision about which retirement account is best suited for your needs.

If you're asking yourself, "What's the difference between a Roth and a Traditional IRA?", you're not alone. Many people find themselves weighing the pros and cons of each option, considering factors such as tax implications, contribution limits, and withdrawal rules. Understanding these differences is crucial in creating a personalized retirement plan that aligns with your financial goals. With the right knowledge, you can optimize your savings and set yourself up for a financially secure future.

As you read on, we will explore various aspects of Roth vs Traditional IRA, including eligibility requirements, tax treatments, and potential penalties for early withdrawals. By the end of this article, you will have a clearer understanding of these two popular retirement accounts, empowering you to make the best choice for your financial future.

What is a Traditional IRA?

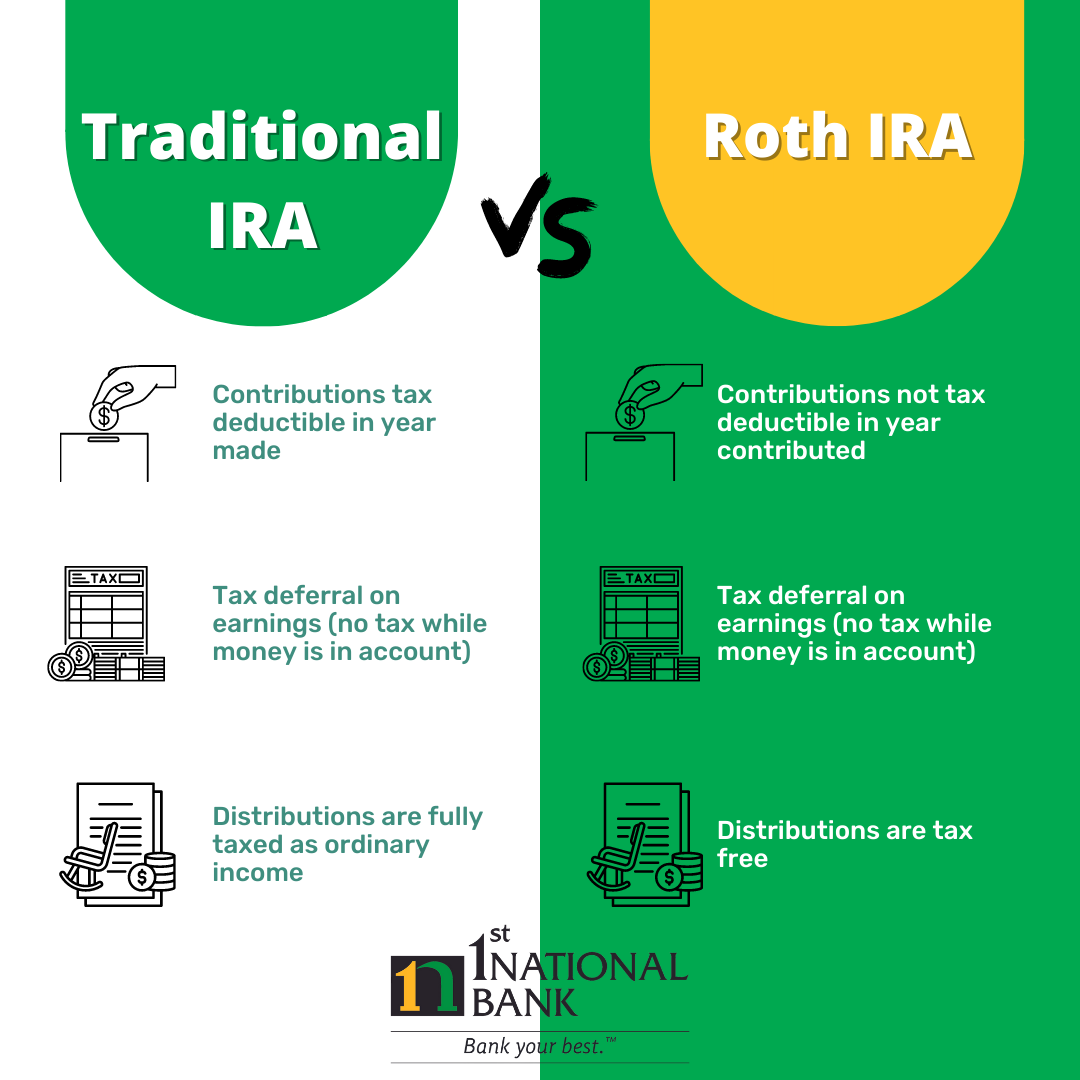

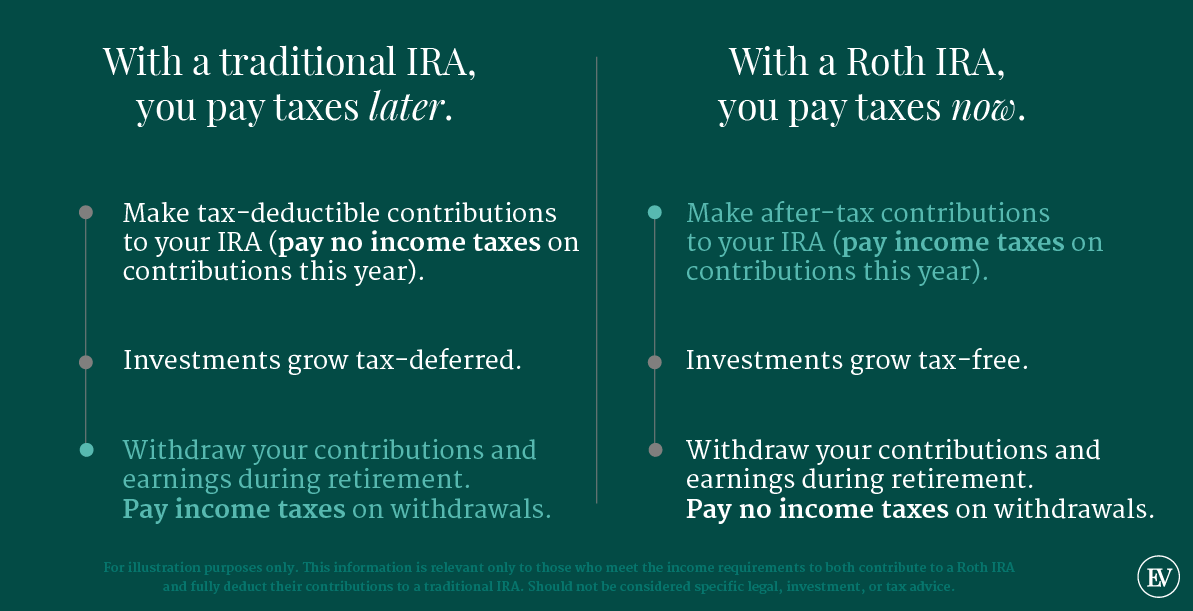

A Traditional IRA is a retirement savings account that allows individuals to contribute pre-tax income, which can lower their taxable income in the year of contribution. This means that you pay taxes on your contributions and earnings when you withdraw them in retirement, typically during a time when you may be in a lower tax bracket. Here are some key features of a Traditional IRA:

- Contributions may be tax-deductible.

- Taxes are deferred until withdrawal.

- Required minimum distributions (RMDs) must begin at age 72.

What is a Roth IRA?

A Roth IRA is another type of retirement account, but it operates differently than a Traditional IRA. Contributions to a Roth IRA are made with after-tax dollars, meaning you pay taxes on the money before it goes into the account. The main advantage of a Roth IRA is that qualified withdrawals in retirement are tax-free. Here are some notable features of a Roth IRA:

- Contributions are made with after-tax income.

- Qualified withdrawals, including earnings, are tax-free.

- No required minimum distributions during the account holder’s lifetime.

What are the Key Differences Between Roth and Traditional IRA?

Understanding the core differences between Roth and Traditional IRAs can help you make an informed decision. Here are the main distinctions:

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Tax Treatment | Contributions are tax-deductible, withdrawals taxed | Contributions taxed, withdrawals tax-free |

| Withdrawal Rules | Penalties for early withdrawal, RMDs at age 72 | No RMDs, contributions can be withdrawn anytime |

| Eligibility | No income limits for contributions | Income limits apply for contributions |

Which IRA is Right for Your Financial Situation?

Choosing between a Roth vs Traditional IRA largely depends on your financial situation and retirement goals. Here are some questions to consider:

- What is your current income level and tax bracket?

- Do you expect your tax rate to increase or decrease in retirement?

- What is your age, and how far are you from retirement?

By answering these questions, you can better assess which IRA may provide the most significant benefits tailored to your unique circumstances.

What are the Contribution Limits for Each IRA?

Both Roth and Traditional IRAs have specific contribution limits set by the IRS. For the tax year 2023, the contribution limit is:

- $6,500 for individuals under age 50

- $7,500 for individuals aged 50 and older (including a catch-up contribution)

It's essential to note that if you are contributing to both types of IRAs, the total contribution across both accounts cannot exceed the annual limit.

What Happens if You Withdraw Early?

Withdrawals from either account before the age of 59½ can result in penalties. However, the rules differ:

- For a Traditional IRA, early withdrawals are subject to a 10% penalty on the amount withdrawn, as well as regular income tax.

- For a Roth IRA, you can withdraw your contributions at any time without penalties. However, withdrawing earnings early may incur taxes and penalties unless specific conditions are met.

Are There Income Limits for Roth IRA Contributions?

Yes, Roth IRAs have income limits that determine eligibility for contributions. For the tax year 2023, the limits are as follows:

- Single filers: Phase-out range begins at $138,000 and ends at $153,000

- Married filing jointly: Phase-out range begins at $218,000 and ends at $228,000

If your income exceeds these thresholds, you may not be able to contribute directly to a Roth IRA, but you can explore a Backdoor Roth IRA option.

How Do You Decide Between Roth vs Traditional IRA?

Deciding between a Roth vs Traditional IRA requires careful consideration of your current and expected future financial situation. Here are some strategies to help you make the decision:

- Evaluate your current tax rate and anticipate what it might be in retirement.

- Consider your age and how long you plan to let your investments grow.

- Analyze your cash flow needs and whether you may need to access your funds early.

Consulting with a financial advisor can also provide personalized insights tailored to your financial goals.

Conclusion: Making the Right Choice for Your Future

In conclusion, understanding the differences between Roth vs Traditional IRA is essential for effective retirement planning. Each option offers distinct advantages that can cater to your specific financial circumstances and goals. By carefully considering your tax situation, income level, and withdrawal needs, you can make an informed choice that sets you on the path toward a secure retirement. Remember that the sooner you start saving, the more time your investments have to grow, so take action today and secure your financial future!