When it comes to retirement savings, two of the most popular options are Individual Retirement Accounts (IRAs) and 401(k) plans. Both of these vehicles offer tax advantages and can help you build a nest egg for your future, but they serve different purposes and have distinct features. Understanding these differences can greatly influence your financial planning and retirement strategy.

Choosing between an IRA and a 401(k) can be confusing, especially with the myriad of options and rules surrounding each type of account. IRAs are typically opened by individuals and offer a wide range of investment choices, while 401(k) plans are employer-sponsored and may come with limited investment options. Both accounts have their pros and cons, making it essential for savers to weigh their options carefully.

In this article, we will dive deep into the world of retirement savings, comparing IRA vs 401k in various aspects such as contribution limits, tax implications, and withdrawal rules. By the end of this article, you will have a clearer understanding of which option might be best suited for your individual needs and circumstances.

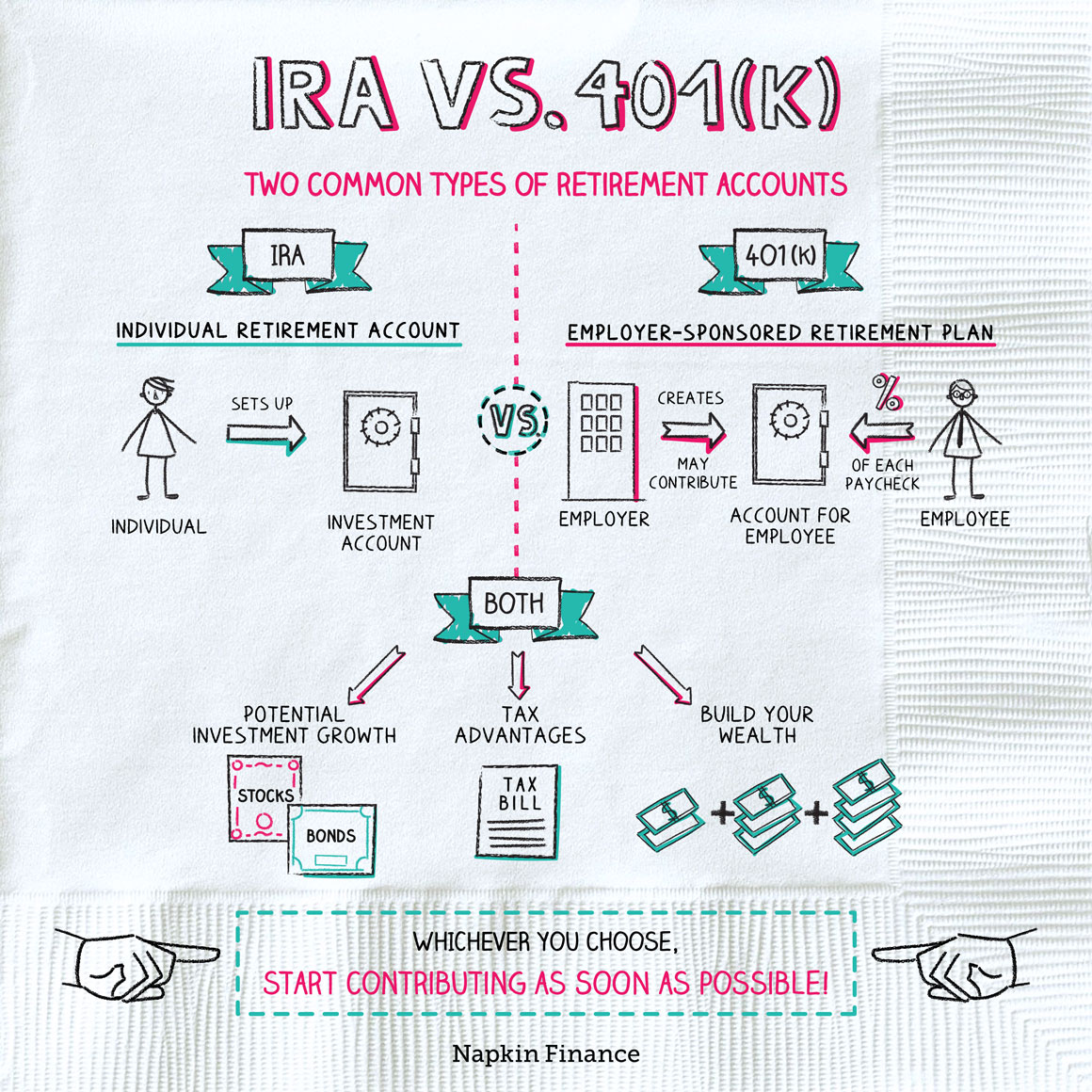

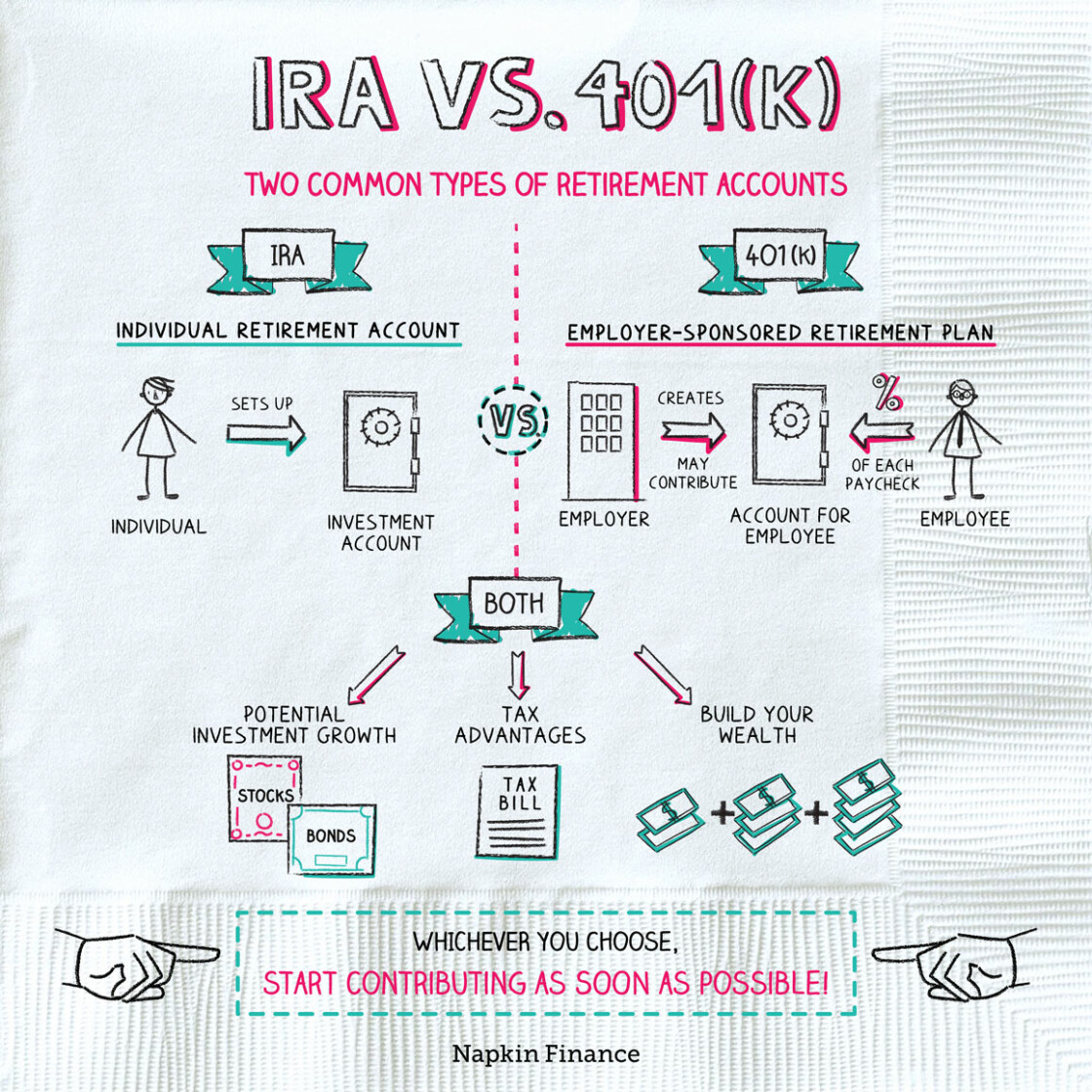

What is an IRA?

An Individual Retirement Account (IRA) is a personal savings account designed to help individuals save for retirement while enjoying certain tax advantages. There are several types of IRAs, including traditional IRAs, Roth IRAs, and SEP IRAs, each with its own rules and benefits. With an IRA, you have more control over your investment choices, as you can select from a broader range of assets, including stocks, bonds, mutual funds, and ETFs.

What is a 401(k) Plan?

A 401(k) plan is an employer-sponsored retirement savings plan that allows employees to save a portion of their paycheck before taxes are deducted. Many employers offer matching contributions, which can significantly enhance the growth of your retirement savings. However, the investment options in a 401(k) plan are typically more limited compared to an IRA, often consisting of a selection of mutual funds and other investment products chosen by the employer.

What are the Key Differences Between IRA and 401(k)?

While both IRAs and 401(k) plans serve the same general purpose of helping individuals save for retirement, there are several key differences between the two:

- Contribution Limits: The annual contribution limits for IRAs are generally lower than for 401(k) plans.

- Tax Treatment: Traditional IRAs offer tax-deferred growth, while Roth IRAs provide tax-free growth. 401(k) plans also offer tax-deferred growth.

- Employer Matching: 401(k) plans often come with employer matching contributions, which can boost your savings.

- Investment Choices: IRAs typically offer a broader range of investment options compared to 401(k) plans.

How Much Can You Contribute to an IRA vs 401(k)?

The contribution limits for IRAs and 401(k) plans vary and can change annually. As of 2023, the contribution limits are as follows:

- Traditional and Roth IRAs: Individuals can contribute up to $6,500 per year, with an additional $1,000 catch-up contribution allowed for those aged 50 and older.

- 401(k) Plans: Employees can contribute up to $22,500 per year, with a catch-up contribution of $7,500 for those aged 50 and older.

What Are the Tax Implications of IRA vs 401(k)?

Tax treatment is one of the most significant factors to consider when choosing between an IRA vs 401k. Here’s how they differ:

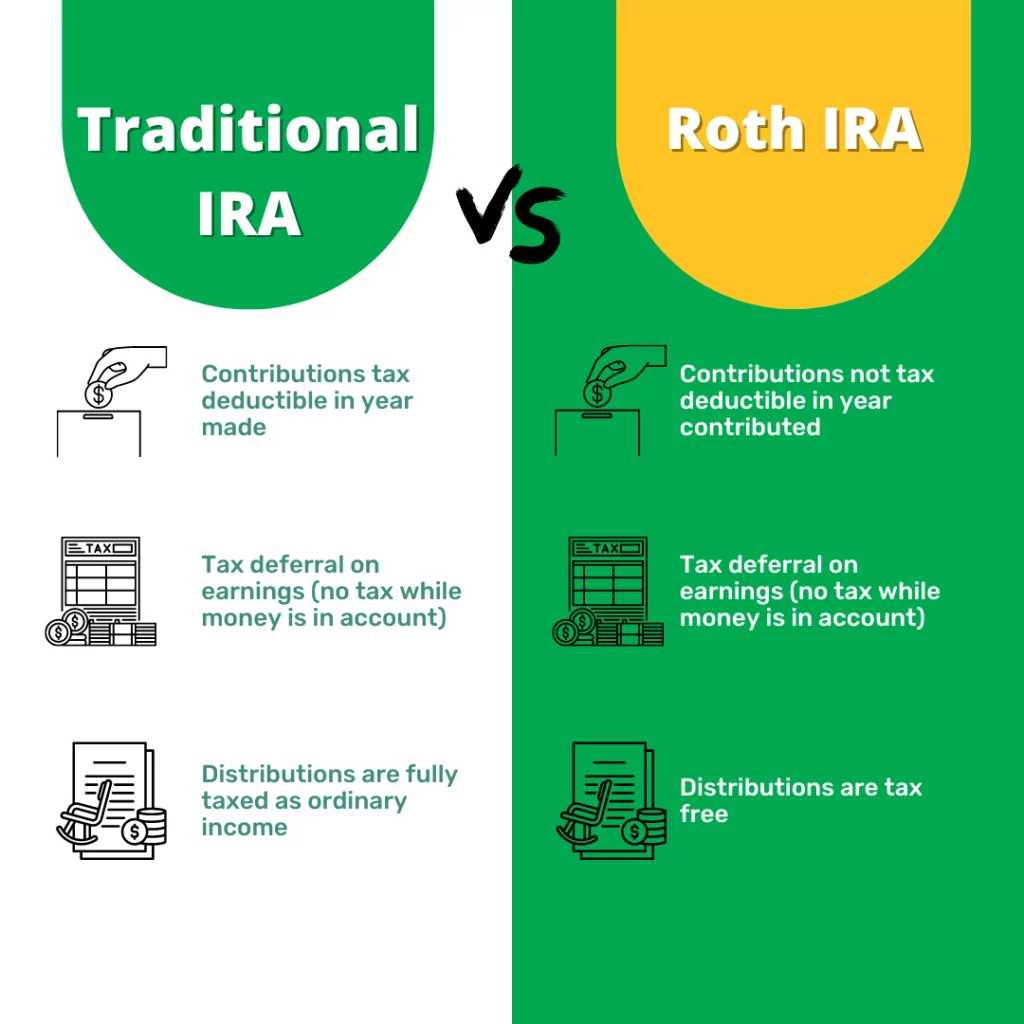

- Traditional IRA: Contributions may be tax-deductible, and taxes are paid upon withdrawal during retirement.

- Roth IRA: Contributions are made with after-tax dollars, allowing for tax-free withdrawals during retirement.

- 401(k): Contributions are made pre-tax, reducing your taxable income for the year, with taxes paid upon withdrawal.

When Can You Withdraw Funds from IRA vs 401(k)?

Withdrawal rules also differ significantly between IRAs and 401(k) plans:

- IRA: Funds can be withdrawn penalty-free after age 59½; however, early withdrawals may incur a penalty unless exceptions apply.

- 401(k): Similar to IRAs, funds can be withdrawn penalty-free after age 59½; however, some plans allow for loans or hardship withdrawals.

Which Option is Right for You: IRA or 401(k)?

Choosing between an IRA and a 401(k) plan depends on your individual financial situation, retirement goals, and employer offerings. Here are some questions to consider:

- Do you have access to an employer-sponsored 401(k) plan?

- Are you eligible for employer matching contributions?

- What are your income levels and tax situation?

- Do you prefer a wider range of investment options?

In many cases, individuals may choose to contribute to both an IRA and a 401(k) plan to maximize their retirement savings. However, it’s crucial to understand the strengths and weaknesses of each option to make informed decisions.

Conclusion: Making an Informed Decision Between IRA vs 401k

In conclusion, both IRA and 401(k) plans are valuable tools for retirement savings, each with their unique features and benefits. By understanding the differences between IRA vs 401k, you can make a more informed decision that aligns with your financial goals and retirement plans. Consult with a financial advisor to help you navigate the complexities of retirement planning and choose the best option for your future.