When it comes to financing your education, understanding the types of loans available is crucial. Two common options are subsidized and unsubsidized loans, both of which can help students cover the costs of college. However, they operate under different terms and conditions that can significantly impact your financial future. Making an informed choice between these two options can save you money and reduce your debt burden after graduation.

The primary difference lies in how interest accrues. For subsidized loans, the government pays the interest while you are in school, during the grace period, and during deferment periods. In contrast, unsubsidized loans begin accruing interest as soon as the funds are disbursed, meaning you are responsible for all the interest from the start. This fundamental difference can affect the total amount you eventually repay.

As you navigate your educational financing options, it's essential to weigh the pros and cons of subsidized vs unsubsidized loans. Understanding your eligibility, the impact on your financial situation, and how these loans fit into your overall education funding strategy will empower you to make the best choice for your future.

What are Subsidized Loans?

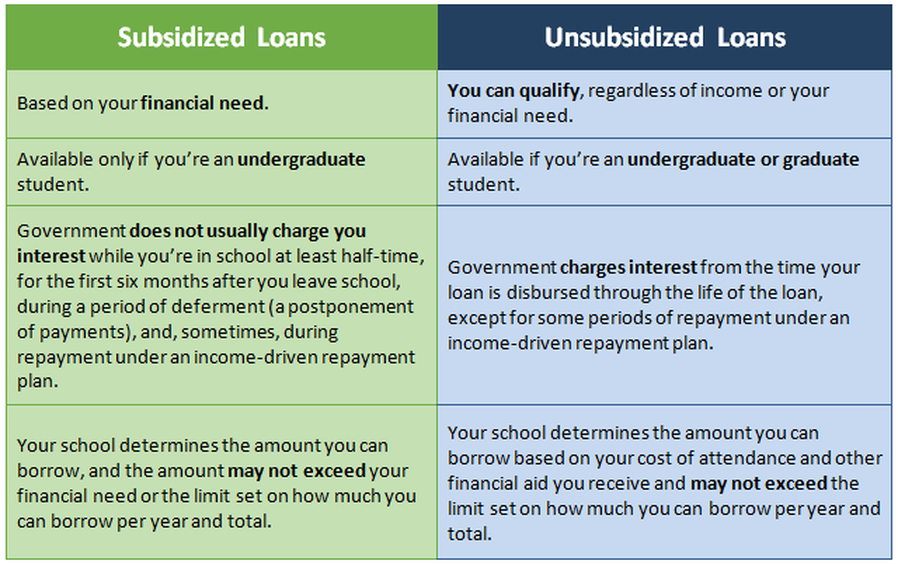

Subsidized loans are a type of federal student loan offered to eligible undergraduate students who demonstrate financial need. The key feature of subsidized loans is that the government covers the interest while the borrower is enrolled in school at least half-time, during the grace period, and during any deferment periods. This can make a significant difference in the total amount repaid over the life of the loan.

Who is Eligible for Subsidized Loans?

Eligibility for subsidized loans is determined by the Free Application for Federal Student Aid (FAFSA). To qualify, students must demonstrate financial need, which is calculated based on their cost of attendance, expected family contribution, and other financial aid received. It’s important to complete the FAFSA as early as possible, as funds are limited.

What are the Benefits of Subsidized Loans?

- Interest Coverage: The government pays the interest while you’re in school, reducing your overall debt.

- Lower Total Cost: Since interest doesn’t accumulate while you’re in school, you can save money over the life of the loan.

- Flexible Repayment Options: They often come with more favorable repayment terms compared to other loans.

What are Unsubsidized Loans?

Unsubsidized loans are also federal student loans, but they do not require demonstration of financial need. Unlike subsidized loans, interest begins to accrue as soon as the loan is disbursed, regardless of the borrower’s enrollment status. This means that while you can take advantage of unsubsidized loans without demonstrating financial need, the total cost of borrowing can be significantly higher.

Who is Eligible for Unsubsidized Loans?

Any student who is eligible for federal student aid can apply for unsubsidized loans, regardless of financial need. This makes them accessible to a broader range of students, including graduate and professional students.

What are the Benefits of Unsubsidized Loans?

- No Financial Need Requirement: Everyone can apply, regardless of their financial situation.

- Higher Borrowing Limits: Unsubsidized loans often allow students to borrow more than subsidized loans.

- Flexible Use: Funds can be used for a variety of education-related expenses, including tuition, books, and living costs.

Subsidized vs Unsubsidized Loans: Which is Right for You?

Choosing between subsidized and unsubsidized loans ultimately depends on your financial situation and needs. If you qualify for subsidized loans, they are generally the better option due to the interest benefits. However, if you do not demonstrate financial need, unsubsidized loans can still provide necessary funding for your education.

How Do You Manage Both Loan Types?

If you decide to take both subsidized and unsubsidized loans, it’s essential to keep track of the different interest rates and repayment terms. Create a repayment strategy that prioritizes paying off the unsubsidized loans first, as they accrue interest immediately. Keeping organized records will help you manage your debt effectively.

What Should You Consider Before Taking Out Loans?

- Borrowing Amount: Assess how much you truly need to borrow.

- Future Earnings Potential: Consider your expected income after graduation and how it will affect your ability to repay loans.

- Loan Repayment Plans: Familiarize yourself with the different repayment options available for both loan types.

Conclusion: Making an Informed Decision

Understanding the differences between subsidized vs unsubsidized loans is essential for any student seeking financial assistance for their education. By evaluating your eligibility, financial need, and future career prospects, you can make an informed decision that aligns with your long-term financial goals. Remember to utilize tools and resources available to you, including financial aid advisors and loan calculators, to navigate your educational financing journey successfully.

:max_bytes(150000):strip_icc()/federal-direct-loans-subsidized-vs-unsubsidized-Final-f0f41bb91a7143fbb1657b8d352c6ae7.png)