The average mortgage rate is a crucial factor for anyone looking to buy a home or refinance their existing mortgage. It serves as an indicator of the overall cost of borrowing money to purchase real estate. Whether you are a first-time homebuyer or a seasoned investor, knowing the average mortgage rate can help you make informed decisions that can save you thousands of dollars over the life of your loan. In today’s fluctuating financial landscape, mortgage rates can vary significantly based on multiple factors including economic conditions, government regulations, and personal financial profiles. Thus, understanding how these rates work and what influences them is essential for securing the best deal possible.

As mortgage rates change over time, it’s important to stay updated on current trends. This knowledge not only helps you gauge the right time to buy or refinance but also aids in budgeting for your monthly payments. With the right information at your fingertips, you can effectively navigate the mortgage market and find the most suitable financing options tailored to your needs.

In this article, we will explore various aspects of the average mortgage rate, including current trends, historical data, and factors influencing these rates. Additionally, we will answer common questions that many prospective homeowners have, providing you with comprehensive insights that can empower your home-buying journey.

What is the Average Mortgage Rate?

The average mortgage rate is the mean interest rate charged on mortgages across various lenders and loan types. It is typically expressed as an annual percentage rate (APR) and can vary based on loan terms, borrower qualifications, and market conditions. Understanding this rate is vital for anyone looking to secure a mortgage, as it directly affects the total cost of borrowing.

How is the Average Mortgage Rate Determined?

Several factors contribute to the determination of the average mortgage rate, including:

- Economic Indicators: The state of the economy, including inflation and employment rates, can influence mortgage rates.

- Federal Reserve Policies: The Federal Reserve’s decisions on interest rates can lead to changes in mortgage rates.

- Credit Score: Borrowers with higher credit scores typically qualify for lower rates.

- Down Payment Amount: A larger down payment can reduce the mortgage rate offered.

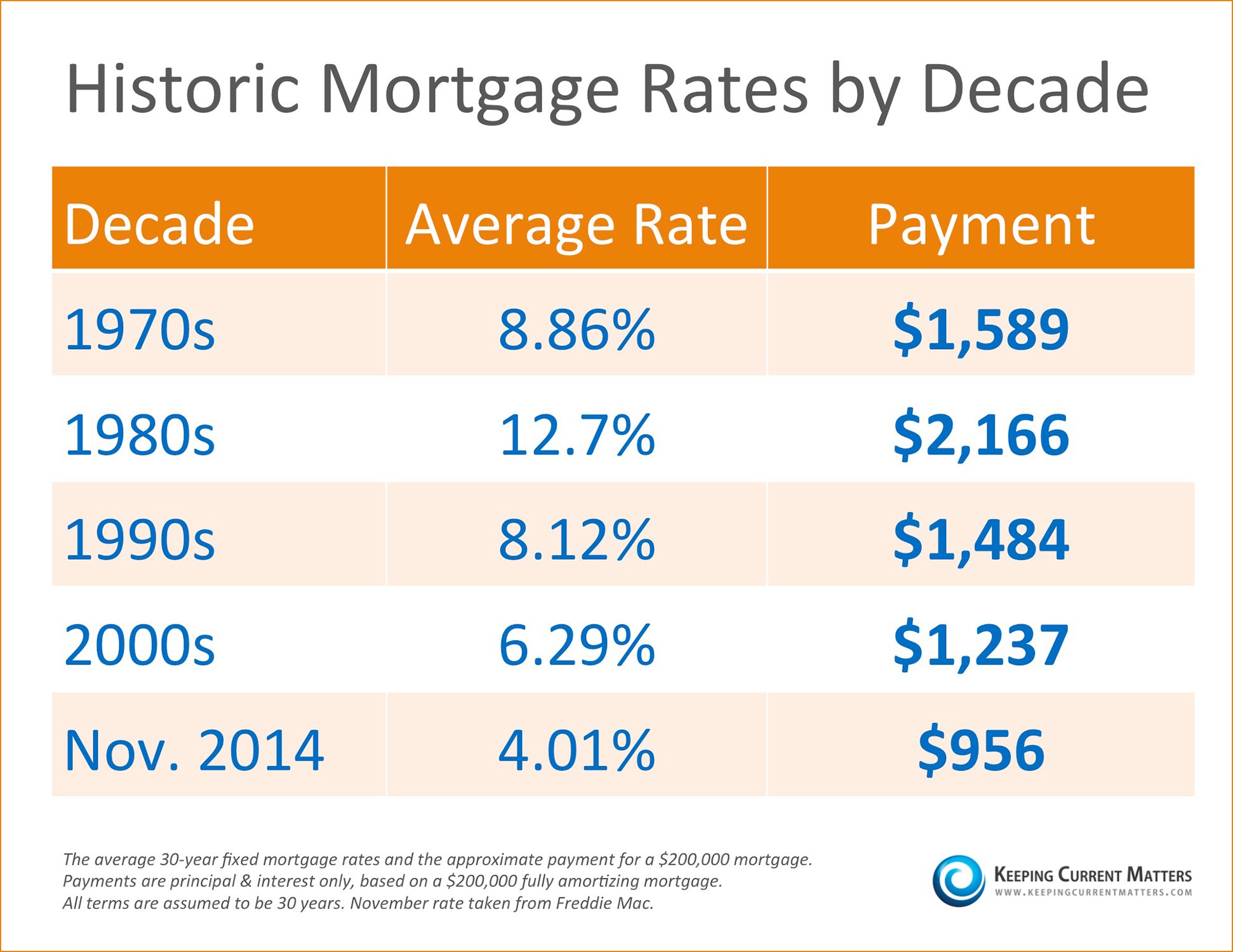

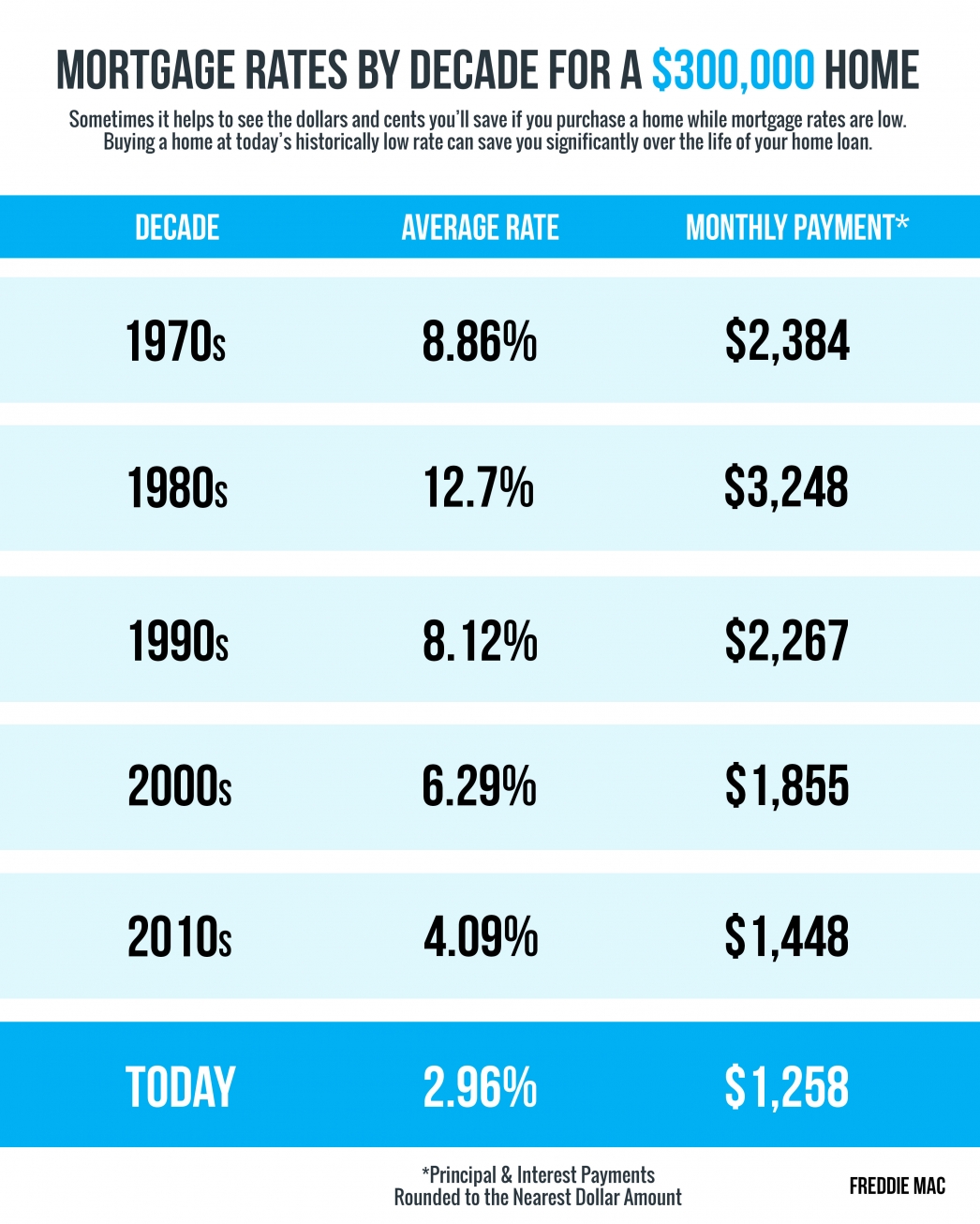

What is the Historical Average Mortgage Rate?

To fully grasp the current average mortgage rate, it's beneficial to look at historical trends. Over the past few decades, mortgage rates have fluctuated dramatically, influenced by various economic cycles, government policies, and market demands. For instance, rates have seen lows of around 3% and highs of over 18% in the 1980s.

How Do Average Mortgage Rates Compare by Loan Type?

Different types of loans may have varying average mortgage rates. Here’s a quick comparison:

- Fixed-Rate Mortgages: Generally offer stable rates throughout the loan term, making them a popular choice for long-term homeowners.

- Adjustable-Rate Mortgages (ARMs): Often start with lower rates but can fluctuate after an initial period, posing potential risks to borrowers.

- FHA Loans: Typically have lower average rates and down payment requirements, catering to first-time buyers.

- VA Loans: Available to veterans, often come with competitive rates and no down payment options.

What is the Impact of the Average Mortgage Rate on Homebuyers?

The average mortgage rate significantly impacts homebuyers in several ways:

- Monthly Payments: Higher rates lead to increased monthly payments, affecting affordability.

- Loan Approval: Lenders may tighten borrowing criteria during periods of high rates, making it harder to qualify.

- Overall Loan Cost: The total cost of the mortgage can increase substantially with higher rates, affecting long-term financial planning.

What Should Homebuyers Consider When Choosing a Mortgage Rate?

When selecting a mortgage rate, homebuyers should consider the following:

- Current Rate Trends: Stay informed about the latest rate changes and market forecasts.

- Your Financial Situation: Assess your credit score, debt-to-income ratio, and financial stability.

- Loan Type: Choose the loan type that best fits your financial goals and risk tolerance.

- Locking in Rates: Consider locking in a rate if you find a favorable one, especially in a fluctuating market.

What Resources are Available for Monitoring Average Mortgage Rates?

Several online resources can help you monitor average mortgage rates:

- Mortgage Rate Websites: Websites like Bankrate and Freddie Mac provide updated average rates.

- Financial News Outlets: Stay tuned to financial news for insights on economic factors affecting mortgage rates.

- Mortgage Lenders: Contact lenders directly for personalized rate quotes based on your financial profile.

Conclusion: How to Navigate the Average Mortgage Rate?

Navigating the average mortgage rate landscape can be complex, but understanding its implications is essential for making informed financial decisions. By staying updated on current trends, assessing personal financial situations, and leveraging available resources, homebuyers can position themselves to secure the best possible mortgage rates. Make sure to consult with financial advisors and mortgage professionals to help you through this important process.